FACT: It has been over 60-years since Canada purchased a submarine. FACT: Canada has never built one. FACT: Currently the Canadian military have ONE operable submarine out of a fleet of four used ones previously purchased. FACT: Canada recently proclaimed themselves as the North American defender of the Arctic.

Now, put all those facts in the overlay of the December 2024 meeting in Mar-a-Lago between President Trump and Canadian Prime Minister Justin Trudeau. President Trump was demanding that Trudeau increase their NATO spending and develop a working Canadian military.

Someone recently asked in the comments section why I have an issue with Canada, specifically why a new level of distain for our Northern neighbors. Quite simply, there is a level of lying that exceeds my tongue bite capacity; that level of deceit comes when fabricating lies is accompanied by pretending. The Canadian government is the worst type of political abuser. They willfully pretend and simultaneously lie to the Canadian people. That’s the answer.

Today, the government of Canadian Prime Minister Mark Carney announce that German industrial shipbuilder TKMS will be awarded a contract for “up to 12 submarines” valued between $20 and $30 billion {source link}. Now, let’s not pretend.

First, the submarine contract is intended to get Canada back into reasonable position on their NATO obligations.

In reality, it is quite remarkable to think about the Canadian nation with only one currently functional submarine. “Canada hasn’t purchased unused submarines since the 1960s, during the Cold War, and has never ordered anywhere near 12 at once. Canada currently owns four subs, all of which were purchased second-hand, and only one of which is typically operational.” {citation} Now, think about that Mar-a-Lago conversation again.

Second, Canada can’t build their own submarines?

Wait, I’ve been told my statements about the absence of Canadian industrial capacity were mistaken. I’ve been told that Canada can produce heavy industrial equipment, and my statements about their heavy industry as functionally obsolescent were overstated. I’ve been criticized for saying that Canada has deindustrialized their economy in the past 30+ years because they have worshipped the altar of “global warming” or “climate change.”

Those two points above are directly connected, and those are the exact points that President Trump was talking to Justin Trudeau about very strongly.

Trudeau said there was no possibility of correcting this industrial lack of ability, and the U.S would just have to accept Canada’s high-horse pontificating position. That’s the core of the 51st state counterpoint.

[NOTE: You cannot have an industrial economy without the ability to create iron, steel, aluminum and various compounds of molten metal. You cannot make metal with windmills, solar or nuclear energy. You must generate massive amounts of heat. That heat is measured in joules because joules are the measurable unit for energy, and they provide a universal, precise way to quantify the energy transferred as heat. Industrial manufacturing takes joules, which creates carbon emission in the process.]

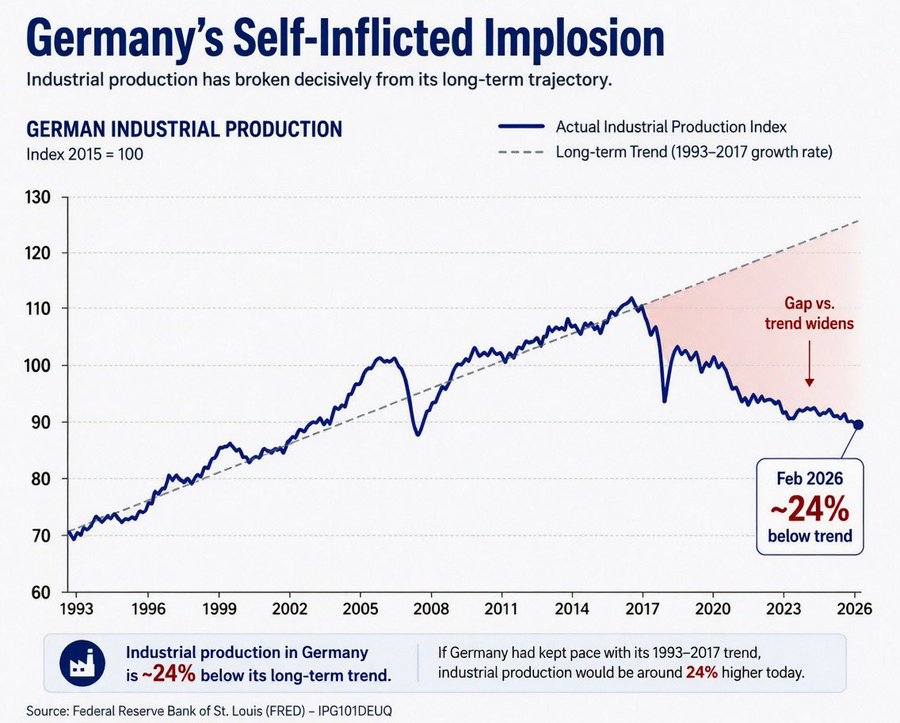

Keep in mind, the USMCA (CUSMA) is going to get terminated. As a consequence, it is easy to see the U.K and EU trying to provide the financial backstop to protect Canada (a commonwealth action). What Carney is doing with this submarine contract is offshoring $30 billion CAD to Germany at current rates, so that Germany can (a) offset their own industrial economic implosion; and (b) position to return a financial favor in the near future.

GERMANY – […] As panic spreads among German manufacturers, layoffs are rolling through formerly prosperous towns and villages with no living memory of a downturn. The moment could become a political turning point for a country whose wealth was largely created by the Mittelstand, or “middle-class”—shorthand for the inner core of Europe’s largest economy.

For the first time in decades, Germany now imports more advanced capital goods from China than it exports there. Manufacturers are suddenly on the defensive, not just in China and elsewhere, but also at home. (more)

Remember the “coalition of the willing” that Mark Carney injected himself into? The U.K, Germany, France and now Canada. They swim together or sink alone.

Oh, things are going to get really ugly. We underestimate when we say, “there are trillions at stake.”

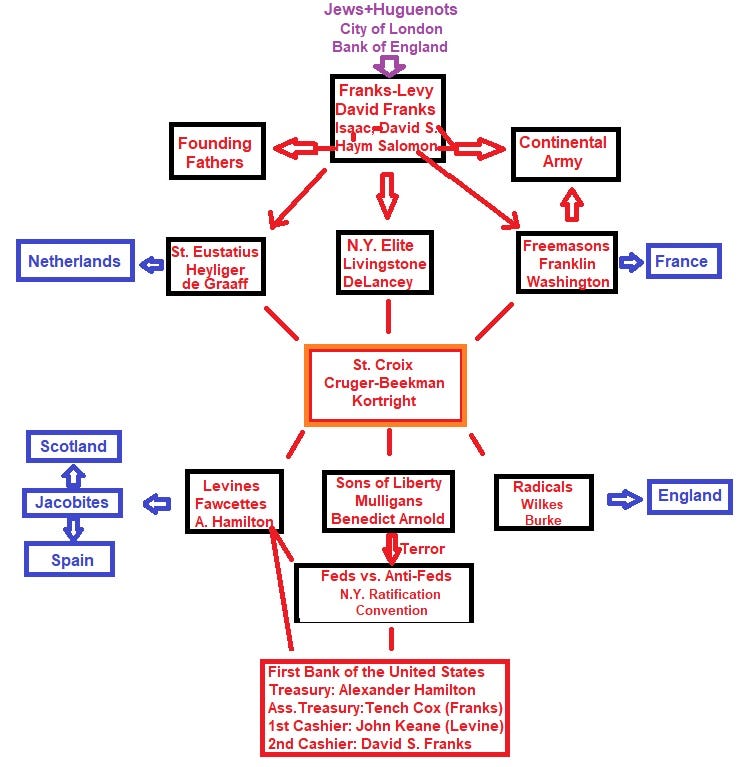

Alexander Hamilton’s Secret Jewish Family, Patrons and Mission

Image: Summary of the article emphasizing the banking and geopolitical aspects of the American Revolution.

Thesis: Alexander Hamilton served as a crypto-Jewish instrument of the Jewish Franks dynasty in the long-term Jewish “master plan” of transforming America into the philosemitic safe haven and power center of the diaspora through the creation of the American central bank.

Introduction

With the 250-year celebration of America’s independence, interest in the Founding Fathers has greatly increased. However, there is one taboo that has stood the test of those 250 years: Alexander Hamilton’s possible Jewishness and the Jewish origins of the American Revolution and USA. This topic is still often treated as a “Nazi conspiracy theory.” However, perhaps understanding American history requires looking through the lenses of both liberty and ethnicity.

The Austro-Libertarian economist and historian Murray Rothbard famously argued that America was conceived in liberty.

This new frontier emerged largely unburdened by government taxes and monopolistic regulations, setting the stage for a vigorous intellectual contest between proponents of small and big government.[2] This ideological struggle has been vividly embodied by two opposite Founding Fathers: Alexander Hamilton and Thomas Jefferson. This intellectual divide has also manifested among historians, with advocates of expansive government championing Hamilton, while defenders of limited government extol Jefferson.[3]

Both camps agree that Hamilton was the architect of the U.S. government and financial system, yet they evaluate his legacy in diametrically opposed ways.

UPDATE: This is the best short explanation of what Trump and his administration are doing. It’s a must view if you want to understand USA. You can read into ‘the British System’ what you want, meaning who controls that? Despite the many distractions in the world today, Trump appears to be resolutely pursuing revitalization of the American System. For this reason alone, he is worth supporting. Elites that profit most from the ‘British’ System will be the ones who complain the most and who spend the most money advertising their POVs. So beware of who is saying what and who is paying for it and what they really want. Go USA! ABN

Not long after July 20th. Sometime within the first two weeks of August is highest probability.

However, it depends on how far out on the ledge cult leader Mark Carney is willing to take his believers. We will enter the ‘Trump playing with them’ phase, just like Trump played with them in Jan, Feb, March ’25 over the 51st state stuff….. Trump will create turmoil, because he holds all the cards for when he triggers the next sequence of events.

Essentially, the landscape is already set up. The bleachers are already built. The venue is already selected…. The Canadians have no concept of it.

At a point determined by Trump he will invite them into the gauntlet. There is no escape and only one way in.

Carney sits down at the table, Trump announces his demands, Carney balks, Trump glances to Greer, Greer hands Carney the formal exit paperwork and then suddenly everyone around Carney realizes what just happened. Trump set up a CUSMA trap.

A six-month countdown clock now ticks loudly. Trump repeats his demands. Carney looks around at his trade delegation, then asks for a few moments. They leave to huddle….

In the Canadian conference room, someone tells the group a six-month exit is now active. The walls are slowly closing.

If no terms are accepted, in six months all U.S. trade with Canada is immediately laissez-faire, no trade agreement backstops anything, meaning every trade is subject to the sectoral whims of the USA commerce department to outline the terms.

Carney asks his team what is happening. Trump tells them to take all the time in the world to think about it, and to give Jamieson or Howard a call if they have questions.

Trump and Greer then hold a press conference, telling the world the formal exit paperwork has now been issued. However, the U.S and Mexico already have a bilateral deal outlined and ready to begin, so U.S-Mexico trade is seamless. The only issue is Canada.

The following day analysts, economists, banking and finance experts begin running the numbers for Canada…… A slow and unstable Canadian economy collapse begins first with a run on the banks by Canadian dollar holders. Everyone needs to buy USD.

Europe and the U.K try to step in to assist by buying Canadian bonds….. but the risk is astronomical.

75% of Canada’s economy is based on trade that is now uncertain.

Suddenly the team around Carney look at things differently. They realize Canada doesn’t sell 75% of their output to the USA; the USA buys 75% of Canadian output.

In every economic relationship, the seller has no leverage. All leverage belongs to the buyer.

The seller can sell anything, but without buyers they are nothing. In a laissez-faire system suddenly U.S. buyers start to dictate terms and prices. The seller has no option. Life inside Canada is FUBAR.

The Chinese move quickly, buying up Canadian holdings for pennies on the ever-diminishing CAD.

Why? Because the Canadian identity is defined by their main focus on ‘not being American.’ It’s all they know.

I can tell you specifically how it will materialize if you want, because I have already gamed this out. You might even make some money if you pay attention.

Toyota and Honda will do exactly what they have said they will do and exit Canadian manufacturing.

With full approval by Carney and the Canadian government, BYD and Geely will step in, purchase and take over those manufacturing plants to create vehicles in Canada (pennies on the CAD).

Canada will cheer because they will believe they just saved all those auto sector jobs. However, a few reality months later and suddenly it is all Chinese industrial operations bringing in Chinese workers to retool the factories.

Canada will end up paying unemployment benefits to Canadian workers, while Chinese factory workers prepare the facilities to manufacture BYD and Geely autos. The Canadian people will grit their teeth, yet do nothing because they accept their provincial government has already been corrupted by Chinese money.

Trump has made a U-turn. Instead of his usual TACO [Trump Always Chickens Out], he chose TITS – Trump Illustrates Terrific Sanity, as said an internet wit. He switched off the Purim War Against Iran, like a housewife turning off her gas stove. The wily Iranians followed Trump’s U-turn, ensuring it’s actually done. The most important result of this debacle: the frog of Israel that tried to compete with the ox of Iran had burst, as Aesop predicted. Israel really believed in his own fairy tale of superiority, of its world hegemony, of its control over the US, until reality came into the picture and slapped its face. Israel has actually been forced to cease killing the Lebanese people. This is a great historical turning point, giving us yet another opportunity to wake the world from its Hollywood fantasy of eternal Jewish might and eternal Jewish victimhood.

It’s not the first event of this kind. Many times, Jews have been stopped just at the brink of total victory. “Keshekvar kim’at”, – in the words of an Israeli song: you always ruin it when we’ve almost won. Putin ended the Seven Bankers’ Rule, by jailing the richest and most powerful of them, oil king Khodorkovsky, and exiling two others, media-lords Berezovsky and Gusinsky. Stalin ended the Jewish Terror by imprisoning the head executioner, Interior Minister Yahoda, and dismissing Foreign Minister Litvinov. So much about Jewish dominance in Russia, as some of the readers claim.

Perhaps we should explain the special Jewish role in empires. The Jews were for hundreds of years traditionally compradors or middlemen; meaning they served their foreign masters and extracted goods from the natives. In long gone times, they served their Polish landlords by forcing the Ukrainian peasants to work harder. It was said (by Jewish historians, of course) that Jews squeezed six times more wealth out of the Ukraine than the Poles ever could. When Western Europe was getting recolonised by the US after WW2, Jews switched to serving the US – but still making the natives miserable. When East Europe was subjugated by the USSR (after its liberation from the German rule), the Jews there served the USSR and ruled over the natives on behalf of the Soviets. They were so awful that the natives rebelled, as in Hungary in 1956, or expelled the Jews, as in Poland in 1967. Thus, Jews have always been a subsidiary force that always hoped to seize the commanding heights – and always failed.

All the important countries of Western Europe were subjugated under US rule after the WWII. Along with the US army came the Jews, as the bearers of the new American policies. The Jews added two techniques particular to them in the process of colonisation. One, de-Christianisation, as Jews traditionally are strongly anti-Christian. Two, encouragement of mass immigration. The Jews had a valid reason to prefer it. In the normal European order of things, the Jews (and Gypsies) stuck out as foreign element. However, in multicultural Europe, Jews would be only one of many different communities.

My most charitable understanding of Trump, especially in the Middle East, is the highlighted paragraph above. This appears to be exactly what he has been doing. It’s a classic Trump move. Shamir’s discussion of the Jewish role in Western history is well-stated and not new. It has also served as an ex post facto excuse for bad Jewish behavior, paired as ever with their false claims of victimhood. That said, if Trump’s actions in the ME and elsewhere are signaling a weakening or end to Jewish control over Western policy, we all should rejoice, including all sane Jews. ABN

Israel is turning on its last important ally in an act of suicidal hubris.

Israel is sabotaging the negotiations with Iran and alienating its last important ally by refusing to halt its attacks on Lebanon and withdraw from its occupation of the south. It is determined to reignite a regional conflagration that could see Iran perpetually close the Strait of Hormuz and plunge the global economy into a global depression. And it continues its genocide in Gaza.

Israel is contaminated by racism and genocidal violence. It is blinded by a repugnant moral superiority. It is corrupted by a class of Zionist billionaires in the U.S. who use their wealth to bend foreign policy to serve Israeli interests. It is equipped with a nuclear arsenal Israeli officials have repeatedlythreatened to use.

It is a menace to the region. It is a menace to itself. And it is a menace to us.

…Israel’s vision of a “Greater Israel,” designed to ensure Israel’s military dominance throughout the Middle East, depends on harnessing the wealth and military power of the U.S.

Over two-thirds of the major arms and munitions Israel imports — without which it could not carry out its genocide of the Palestinians, turn southern Lebanon into a moonscape and bomb Iran, Syria and Qatar — are manufactured and provided by the U.S. And because the Israel lobby, for decades, has owned Congress, because its Zionists allies police and control the media, because it is able to siphon tens of billions of U.S. taxpayer dollars to sustain its military adventurism, Israel is blind to its own limitations. It is willing to inflict harm on its allies, including the U.S., in service to itself.

…Israelis, intoxicated by the fantasy of being the chosen people, do not have friends. They do not have allies. They have those they use and those they slaughter.

The game is up. The Israeli domination of the U.S. political system is coming to an end. Israel’s inability to read U.S. and global opinion — or its own population, where over 90 percent believe Israel lost its war against Iran — along with its stubborn belief that its old levers of power can still work, illustrate a leadership that has rendered itself deaf, dumb and blind. It can and will do a lot of damage. It can and will inflict more death and suffering. But it is cannibalizing itself.

Hedges refers to ‘the obtuse administration of Donald Trump’ and blames much of what is happening on Trump and his admin. He could be right. Many will agree. I see another possibility, which is Trump has given Israel what they wanted and also enough rope to hang themselves. If policy is judged by its outcome, so far Trump’s policy has allowed Israel to show ‘It is a menace to the region. It is a menace to itself. And it is a menace to us.’ I am a pragmatic conservative who understands we are living in an oligarchy and have been for at least 100 years and probably since forever. Weighing Hedges views against that, leaves me in an agnostic state, a position I am very comfortable with because almost everything, including politics, is so full of unknowns, I see no other tenable position. Hedges doesn’t know what Trump and his faction are thinking or doing and neither do I. No one knows anything for certain. And not just in this case but in virtually all cases. This is a main reason, I see zero reason to get excited or inflamed over almost anything. That said, the world is a fascinating place and I remain fully interested in all of it. ABN